Owning Real Estate can be very Profitable, However it is not for everyone.

4 Things you should know:

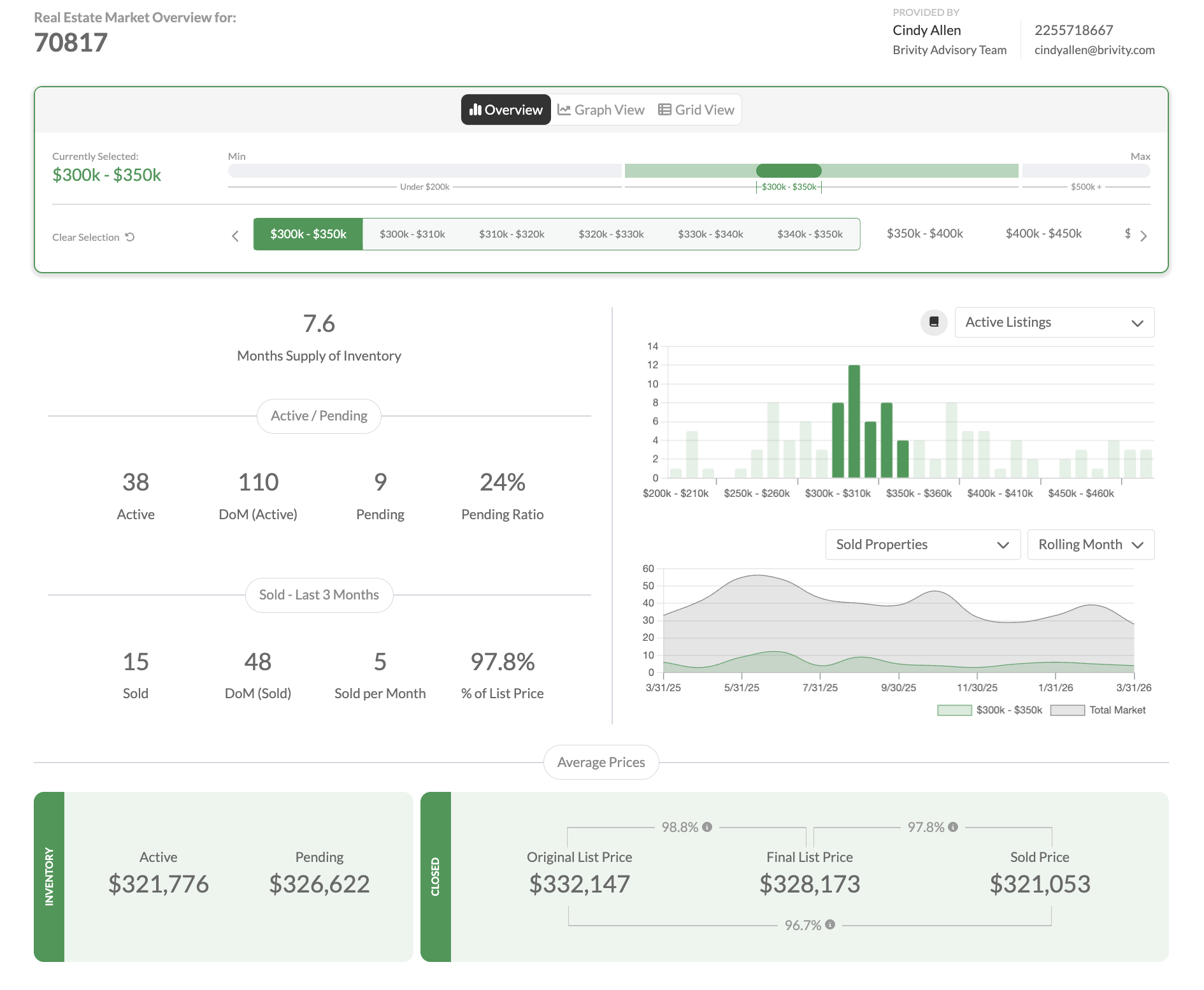

Vacancy Rates

Unless you are using an FHA-backed loan to purchase a condo, you'll never consider vacancy rates when purchasing a residence in which you intend to live. When purchasing rental property, on the other hand, those numbers are critical.

One of the first questions to ask yourself is whether or not you are financially able to pay the house payments when the house sits vacant. Savvy landlords build an emergency fund that they'll tap under these circumstances. Without such a fund, will you be able to cover the payments until you find a tenant?

In October of 2013, for instance, the nation's apartment vacancy rate was the lowest it had been in more than a decade, according to a Reuters news report. This is akin to a seller's market in the residential real estate market – a great time for landlords, with lots of renters in the marketplace. Additionally, when demand for rentals is high and the supply of rentals is low, rents tend to rise.

Because all real estate is local, don't rely on national statistics. This is where a good real estate agent comes in handy. Ask yours to check the vacancy rates for the local market – both current and historic.

The past and current market, however, should never be the sole yardsticks used to measure whether you should get into the landlord business. Check the new construction plans for the area. A surge in new rentals will lift the vacancy rate and slow down the rise in rents.

Laws and Protecting Yourself

Landlords have certain duties, outlined by both federal and state law, including fair housing laws and how to handle rents and deposits. Bone up on your responsibilities and liabilities before agreeing to purchase a rental property. Your attorney can help you with this.

Once you understand this aspect of being a landlord, you'll need to ensure that you understand the lease paperwork. Leases aren't worth the paper they're written on if they disallow you from litigating against a tenant that violates the terms. Again, this is something your attorney can assist with.

Even armed with maximum information, something may go wrong. Talk to an insurance agent before purchasing income property to determine how much insurance you'll need and how much you can expect to pay.

Tax Ramifications

While you'll be taxed on rental income, associated expenses can be deducted on your return.

Deductions are defined as "the ordinary and necessary expenses to manage, conserve, and maintain your property," according to the tax experts at Jackson Hewitt. Deductible expenses include, but aren't limited to:

Cleaning equipment and supplies.

Advertising costs.

Real estate taxes.

Insurance costs.

Mortgage interest paid.

Payments made to maintain the property, such as for lawn service, pest control and trash pickup.

Property management fees.

There are many other deductions - and information about deductible losses -- that your tax professional can alert you to.

It's a Labor-Intensive Job

If you don't hire a property manager, being a landlord may take a huge chunk of your time. In fact, many landlords that have gone the self-management route eventually give up, claiming it is a full-time job.

Consider some of the duties you will potentially have to perform:

Dealing with deadbeat tenants, chasing down payments and fielding complaints from neighbors.

Dealing with evictions.

Taking emergency maintenance phone calls at all hours of the day and night.

Rounding up the appropriate tradespeople to perform repairs and maintenance.

Becoming a landlord requires a lot more than buying a house and advertising it for rent, especially if you hope to turn a profit. Work closely with your financial adviser and your real estate agent, and consider all the ramifications.

Fully Updated List of Investment Properties Available in

Baton Rouge

View More Properties Here

No comments:

Post a Comment